In 2017, Sweden announced the development of its own electronic currency, the e-krona. This fiat currency is predicted to streamline the nation to becoming the first cashless society on the planet. But, this fancy new currency is still largely misunderstood by the rest of the world.

So let’s break down some of the myths about the Swedish e-krona, and separate fact from fiction.

The most well-documented misconception about the e-krona is the belief that it will be a cryptocoin. According to Fortunly, the reason for the confusion is because the Riksbank mentioned cryptocurrency and bitcoin when they discussed the e-krona project for the first time two years ago.

The Swedish central bank has learned from their mistake and made no reference to crypto in their second report in 2018. However, many individuals and businesses in the United Kingdom and Ireland did not get enough clarification about the mysterious money’s true nature.

To set the record straight, the e-krona is a Central Bank Digital Currency (CBDC), which is just the digital version of the Swedish krona. The e-krona is fiat money that will be issued by the Riksbank, much like the remaining coins and banknotes circulating in the Nordic nation.

The e-krona will serve as legal tender and will be controlled by a central authority to keep its price stable. Crypto assets, on the other hand, are more of investments than payment instruments.

The Riksbank did not initiate the CBDC concept; it was the Bank of England that pitched the idea. According to a recent IBM report, several other central banks have been studying the feasibility and viability of such digital currencies to possibly replace cash down the road.

Although the e-krona may be the first CBDC to retire its tangible counterpart, many government-backed digital currencies are already in use. The best example is Venezuela’s cryptocurrency: the Petro. It is actually a stablecoin, a cryptocoin pegged to another stable asset. The Petro is backed by oil.

The e-krona offers the best of fiat money and digital cash. But there is one caveat: it requires tools. While anyone with an internet-connected smartphone in Sweden will be able to use the e-krona for payment when it goes live, some people still prefer the old way.

Many Swedes no longer bring cash with them because several establishments do not accept it anyway. But not 100% of the population is enamored with a cashless life.

Furthermore, the Swedish government needs to build sophisticated infrastructure to take its entire economy to the digital landscape by 2023. If the central bank’s system gets hacked, though, the Swedes might lose complete access to their money since they could not store the e-krona in a jar, hide it under the mattress, or keep it in their pockets.

It actually does the opposite. The Riksbank wants to use the e-krona to counterbalance the growing influence of Sweden’s large banks, which control the mobile payment platform, Swish, in the country. In the event of a crisis, the very presence of the e-krona could empower depositors to do a digital bank run when they no longer trust private financial institutions. The availability of relevant central bank money encourages banks to shape up.

The introduction of the e-krona to the global financial world will be an historic moment. It may not impact cash-reliant societies that much, but it will show us whether or not CBDCs can be the true future of money.

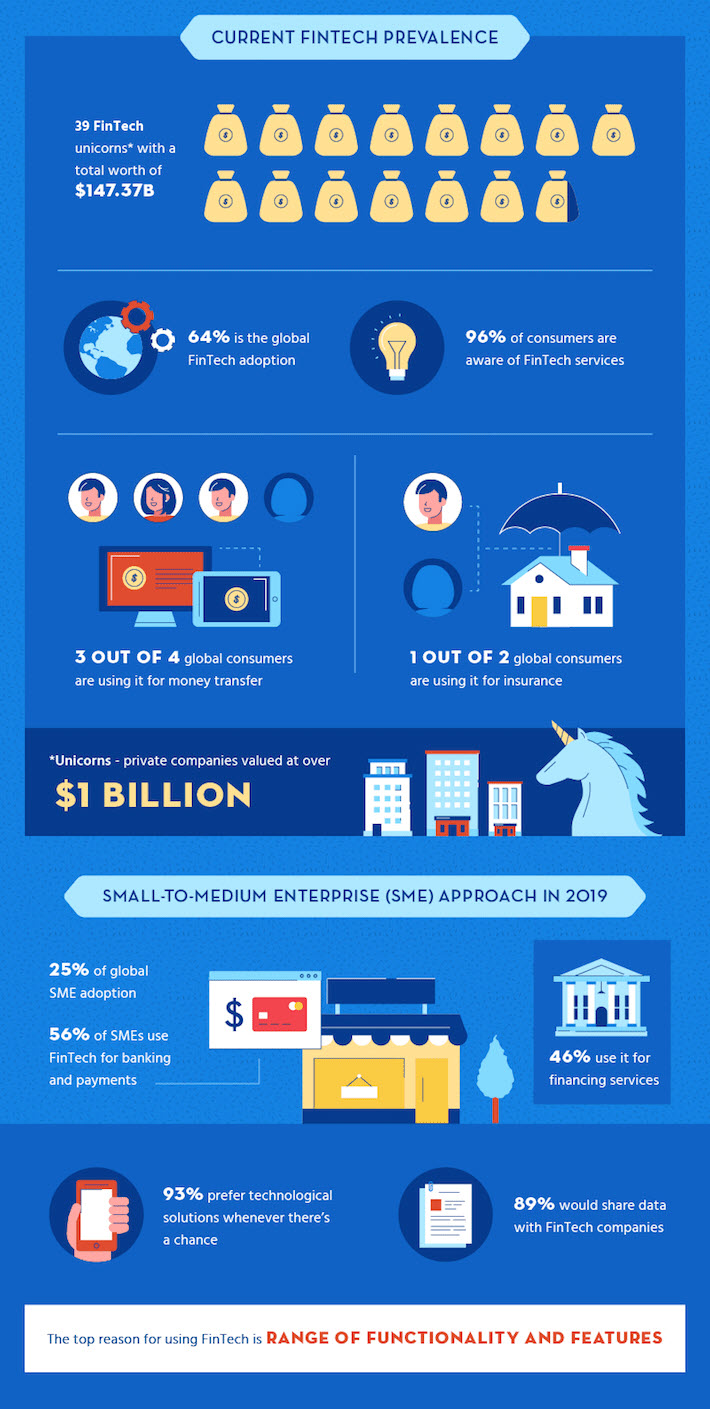

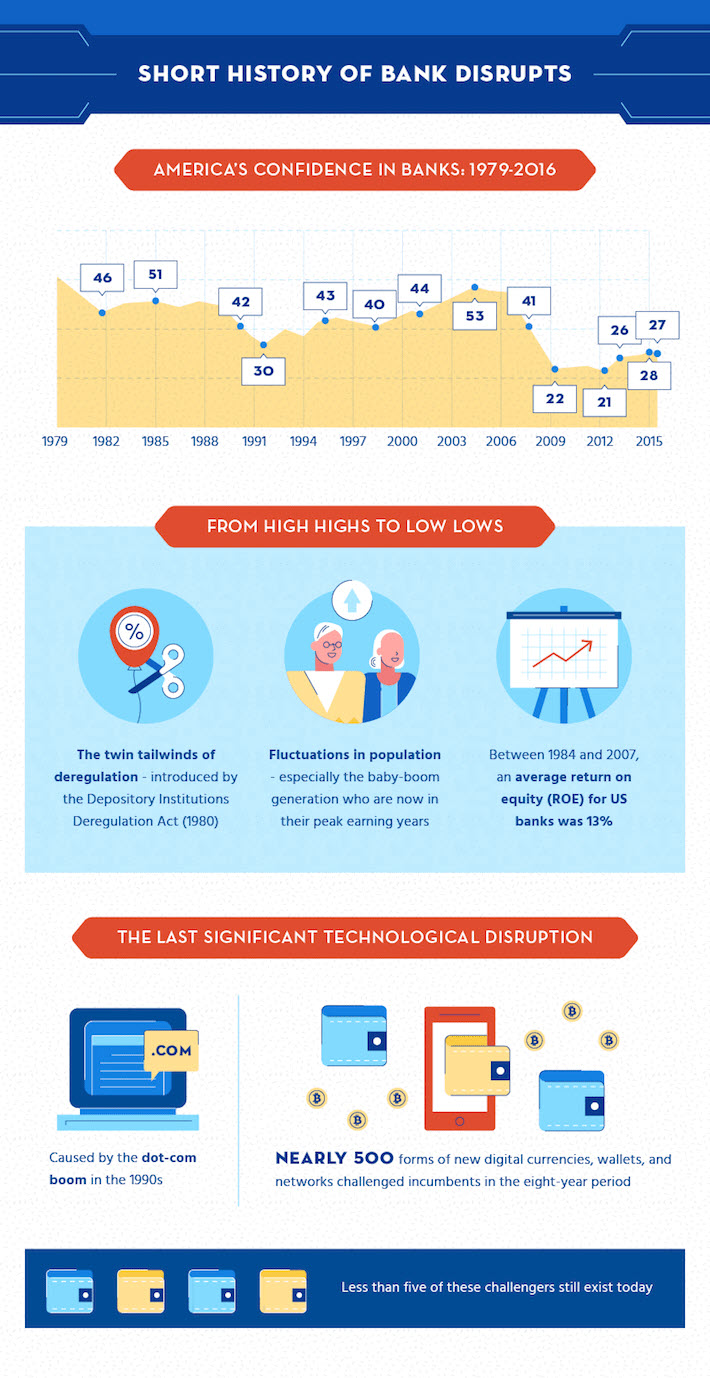

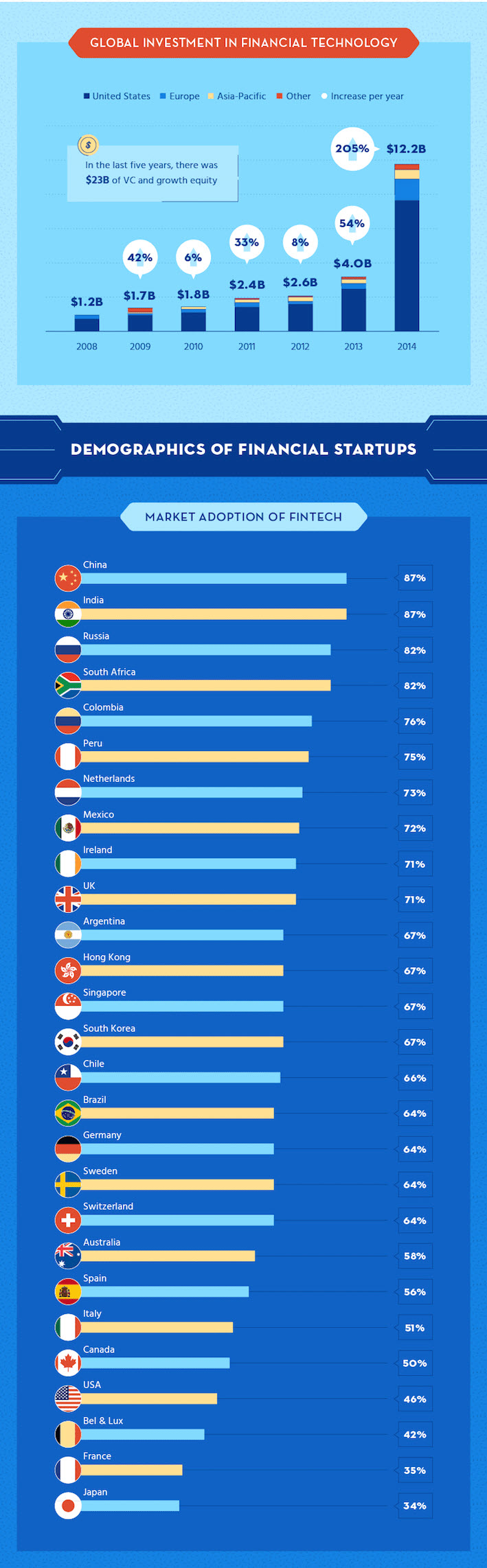

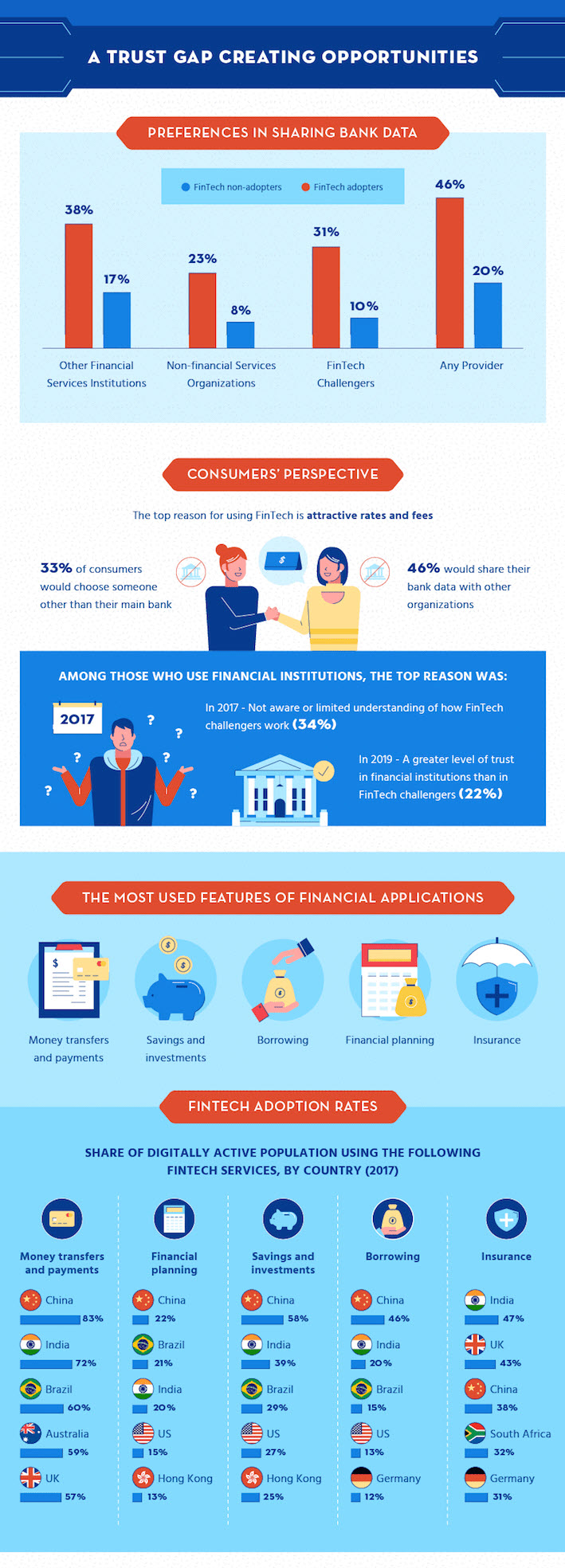

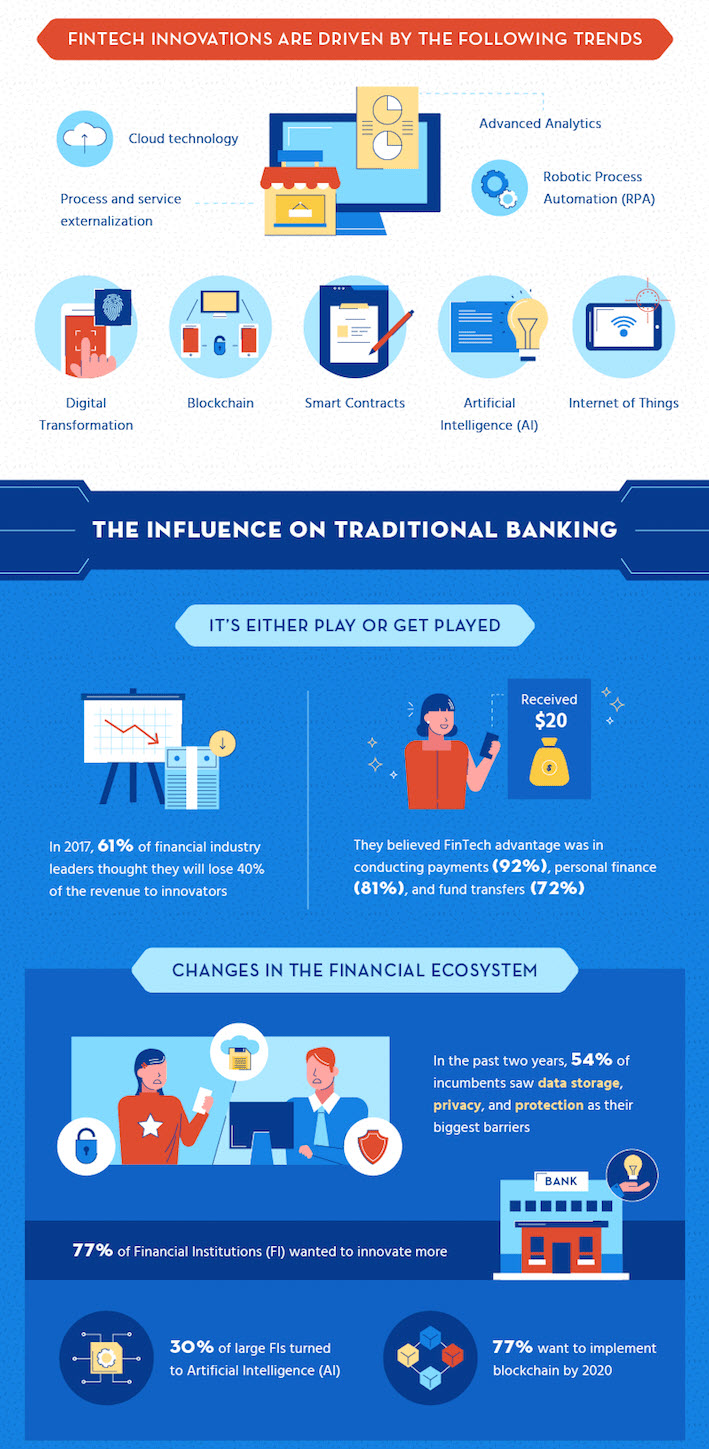

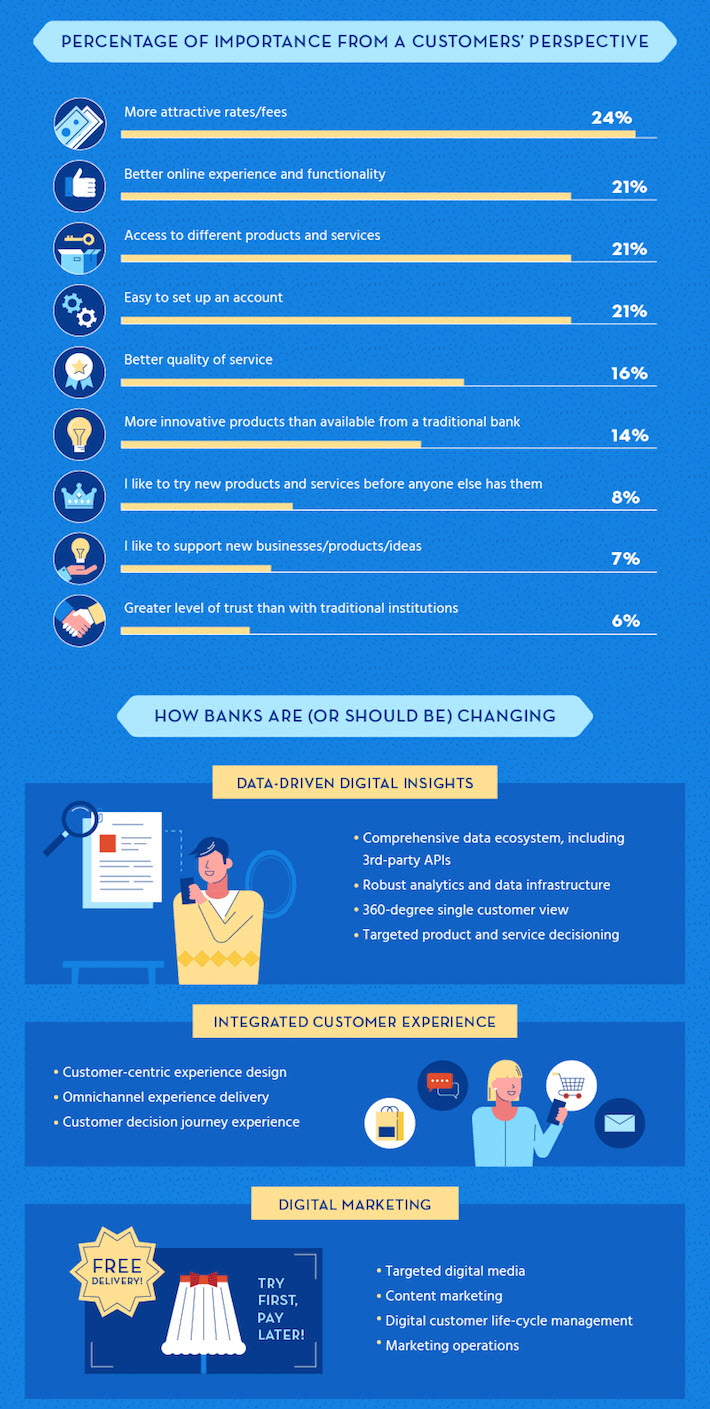

This infographic encompasses all the significant disruptions that fintech solutions are causing in the world of finance. Whether we’re talking about mobile wallets and cashless transaction systems or the rise of blockchain currencies and AI, all the key facts and figures are there.

Title: Today's AI Stories and

Title: Today's AI Stories and

Title: Today's AI Stories and

Title: Today's AI Stories and

Title: Today's AI Stories and

Title: Today's AI Stories and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}